Physician mortgage loans offer several attractive benefits, including low down payment requirements, a straightforward income verification process, and no PMI. These advantages make physician loans an appealing option for many doctors. As a borrower, you might be tempted to buy down your interest rate to lower your overall mortgage costs—but is it really worth it?

Understanding Mortgage Buydowns

A mortgage buydown involves making an upfront payment at closing to reduce your interest rate. This rate reduction is expressed in points, where each point costs 1% of the total loan amount. The more points you purchase, the lower your interest rate will drop. At first glance, buying down your rate might seem like a smart move to save thousands of dollars over the life of your loan.

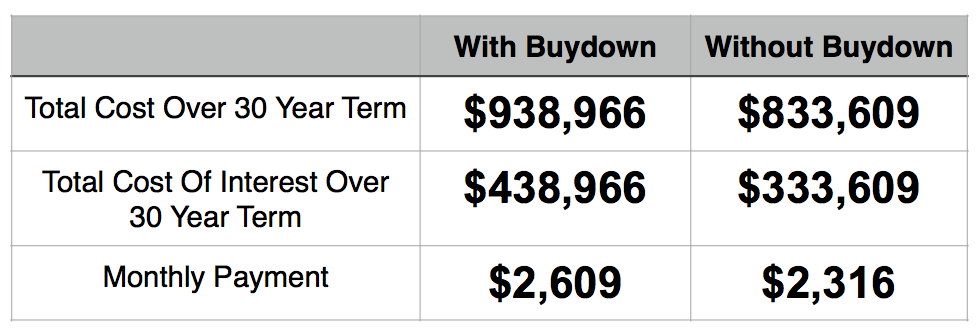

For example, let’s say you qualify for a 30-year fixed-rate physician mortgage of $900,000 at 6.00%. Over the full term, you would repay about $1,942,500. If you decide to buy down your interest rate by one point (which would cost $9,000), your rate could drop by .125-.375%, potentially saving you over $75,000 in interest over the next 30 years. Your monthly payment would also decrease from $5,395.95 to $5,180.91 (assuming 6% vs 5.625%, principal and interest only).

Is Buying Down the Rate Worth It?

While these numbers might sound appealing, it’s essential to consider the broader context—especially in a fluctuating mortgage market. Buying down your rate requires a significant upfront investment, which may not make financial sense for many borrowers, particularly in an environment where interest rates are trending downward.

For instance, if you’re a medical resident or a new doctor, your financial situation might not allow for a substantial cash outlay at closing. Even if you do have the funds available, it’s crucial to evaluate how long you plan to stay in your home. The key metric to consider is the break-even point—the point at which your monthly savings from the lower interest rate equal the cost of the buydown.

In our earlier example, the doctor would need to stay in the home for at least 42 payments (3 years and 6 months) just to break even on the $9,000 spent on the buydown. If there’s any chance you’ll move or refinance before reaching this point, the buydown could end up costing you more than it saves.

Why You Might Want to Avoid Buying Down the Rate

For most borrowers, especially those early in their careers or with plans to move within a few years, buying down the interest rate isn’t usually the best financial decision. Here’s why:

- Upfront Costs: The cost of buying down the rate can be prohibitively expensive, particularly for residents or new doctors who might not have substantial cash reserves.

- Market Trends: In a market where interest rates are expected to decline, locking in a lower rate through a buydown might not be necessary. You could end up refinancing to a lower rate in the future without the need for an upfront payment.

- Short-Term Assignments: If you’re likely to relocate after completing your residency or if your job assignment is temporary, you might sell your home before reaching the break-even point, rendering the buydown a loss.

Financial Flexibility: Rather than tying up funds in a buydown, it might be more prudent to keep that money available for other expenses or investments, particularly if your income is expected to rise significantly in the coming years.

Conclusion: Think Twice Before Buying Down Your Rate

Physician mortgage loans may come with slightly higher interest rates, but that doesn’t mean buying down the rate is always the right move. Established doctors with long-term plans in their current location might benefit from a buydown, but for residents, new doctors, or those with short-term assignments, it’s often better to hold onto your cash and avoid the extra upfront cost.

Instead of focusing on buying down your rate, consider the overall financial picture—how long you plan to stay in the home, the current and projected trends in mortgage rates, and your need for financial flexibility. In many cases, it’s wiser to refrain from purchasing points and instead, allow yourself the flexibility to refinance or make other financial decisions as your career progresses.

For more guidance on making the best financial decisions with your physician mortgage, complete our “Get Started” questionnaire to connect with a lender who can help you navigate your options and find the loan that best suits your needs.